Buying a Bank Auction Property is Risky :

The Bombay High Court Judgement

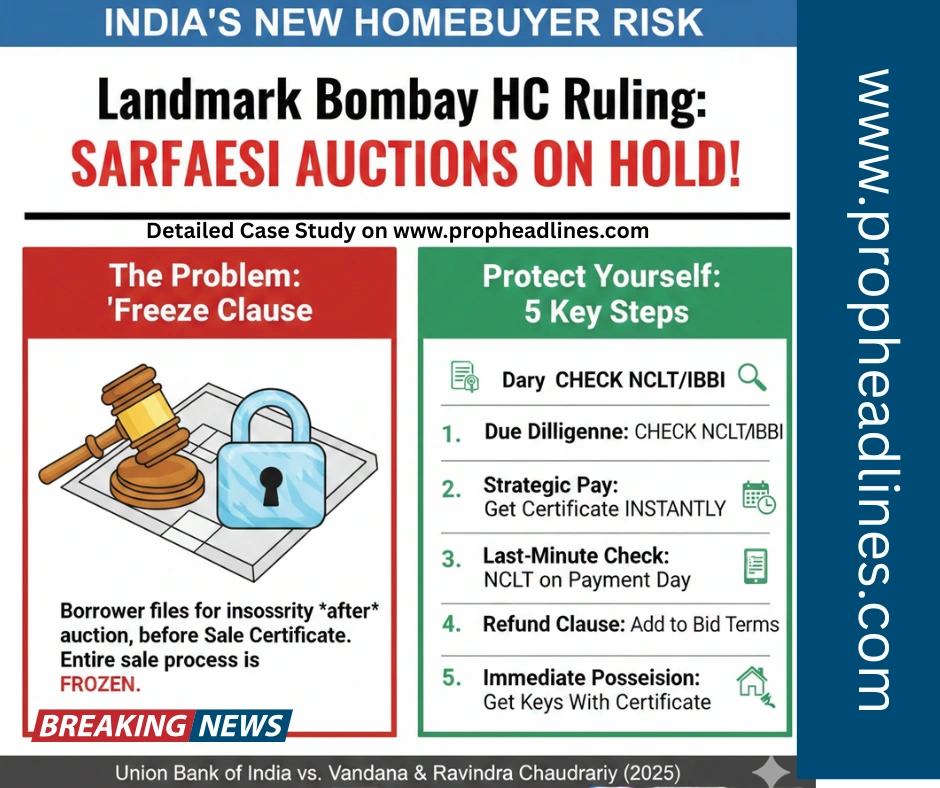

The Detailed case Study of Union Bank of India vs. Vandana and Ravindra Chaudhari

Arrow Business Development Consultants Pvt. Ltd. v. Union Bank of India & Ors.

The case of Union Bank of India vs. Vandana and Ravindra Chaudhari (specifically identified in legal records as Arrow Business Development Consultants Pvt. Ltd. v. Union Bank of India & Ors.) is a significant 2025 judgment by the Bombay High Court.

The case deals with the complex legal interplay between the SARFAESI Act (which helps banks recover bad loans) and the Insolvency and Bankruptcy Code (IBC) (which provides a moratorium or “stay” on debt recovery).

Case Background

The Debt: Vandana and Ravindra Chaudhari (the Borrowers) took loans from Union Bank of India. After they defaulted, the bank classified their account as a Non-Performing Asset (NPA) in April 2023.The Auction: The bank initiated recovery under the SARFAESI Act and auctioned a residential flat in Navi Mumbai. Arrow Business Development Consultants emerged as the successful bidder on May 30, 2025, for ₹9.12 crore.

The Conflict: On June 9, 2025—after the auction but before the sale was fully finalized—Vandana Chaudhari filed for personal insolvency under Section 94 of the IBC. This automatically triggered an interim moratorium under Section 96 of the IBC.

Key Legal Issue

The court had to decide whether a bank can complete a sale and hand over possession to an auction purchaser if an insolvency moratorium begins after the auction is held but before the sale certificate is issued.

The Court’s Ruling

The Bombay High Court (Bench of Justices R.I. Chagla and Farhan P. Dubash) ruled on December 10, 2025, against the bank and the auction purchaser:

Moratorium Takes Precedence: The court held that the interim moratorium under Section 96 of the IBC is "wider" in scope than other sections. It halts all legal actions and proceedings regarding the debt, including the finalization of a SARFAESI sale.Sale Not Complete: A sale under SARFAESI is not considered legally “complete” until the sale certificate is issued and the full payment is processed. Since the moratorium kicked in on June 9 and the sale certificate was only issued on June 20, the bank had no authority to accept the balance payment or finalize the transfer.

No Ownership Transfer: Consequently, the auction purchaser (Arrow Business) did not become the legal owner and was not entitled to take possession of the flat.

Why This Case Matters

This judgment is a landmark for personal guarantors and individual borrowers. it establishes that even if a property has been auctioned, a borrower can effectively “freeze” the process by filing for insolvency, provided the sale has not been fully finalized with a certificate.

How this affects other pending bank auctions or the specific sections of the IBC mentioned?

The Union Bank of India vs. Vandana and Ravindra Chaudhari (2025) case, officially Arrow Business Development Consultants Pvt. Ltd. v. Union Bank of India, has fundamentally changed how banks and auction purchasers approach property sales when a borrower is on the verge of insolvency.

Here is a deeper look into how this ruling affects SARFAESI auctions and the specific IBC sections involved.

- Impact on Future SARFAESI Auctions

The judgment creates a “zone of uncertainty” for banks and auction purchasers between the date of the auction and the final issuance of the sale certificate.

Risk for Auction Purchasers: Even after winning an auction and paying the initial 25%, a purchaser is not guaranteed the property. If the borrower files for insolvency before the final payment is made and the sale certificate is issued, the entire process is "frozen."

Bank's "Due Diligence" Burden: The court noted that banks must now verify if any Section 94/95 insolvency applications have been filed immediately before accepting balance payments or issuing sale certificates. Any money accepted after a moratorium begins might have to be refunded.

"As-is-where-is" No Longer Absolute: While properties are sold "as-is," the court clarified that this doesn't protect a bank from statutory bars like an IBC moratorium. The bank cannot complete a sale once the law (IBC) says all debt-related proceedings must stop.- Understanding Sections 94 and 96 of the IBC

The core of this case relies on the “automatic” nature of the interim moratorium in personal insolvency.

| Feature | Section 94 (Insolvency Application) | Section 96 (Interim Moratorium) |

| Purpose | Allows an individual debtor (or personal guarantor) to apply for insolvency resolution. | Protects the debtor by pausing all debt recovery actions while the application is reviewed. |

| Trigger | Triggered by the filing of the application by the debtor. | Triggered automatically the moment the application is filed. |

| Scope | Applies to all “non-excluded” debts (i.e., most bank loans). | Covers all debts of the debtor and stays all pending legal actions regarding those debts. |

| Duration | Lasts until the NCLT decides to admit or reject the application. | Ceases only when the application is admitted (replaced by a formal moratorium under Sec 101). |

- Key Legal Distinctions

The court made two critical clarifications that resolved long-standing debates:

Ownership vs. Redemption: Under a 2016 amendment to SARFAESI (Section 13(8)), a borrower loses the "right of redemption" (the right to pay the debt and get the property back) once the auction notice is published. However, the court ruled that losing the right to redeem is not the same as losing ownership. Ownership only transfers when the Sale Certificate is issued.

"In Relation to All Debts": The court interpreted the language of Section 96 very broadly. It ruled that the interim moratorium doesn't just protect the person; it stays any action "in respect of any debt." This means the bank’s internal process of finalizing an auction is considered a "proceeding" that must stop.- Status of the Auction Purchaser’s Money

A significant takeaway from the judgment is the status of the ₹9.12 crore paid by Arrow Business:

The court did not order an immediate refund because the purchaser hadn't specifically asked for a refund in their initial petition (they were only asking for possession).

However, the court left it open for the purchaser to file a separate legal action to get their money back from Union Bank of India since the sale was declared legally incomplete.a summary of the steps a homebuyer or auction purchaser should now take to protect themselves in light of this judgment?

The 2025 Bombay High Court ruling in Arrow Business Development Consultants vs. Union Bank of India has introduced a significant risk for anyone looking to buy property through bank auctions.

Because a borrower can now “freeze” a sale simply by filing for insolvency—even after the auction is finished—purchasers must change their strategy. Here is how a homebuyer or investor should protect themselves:

- Enhanced Pre-Auction Due Diligence

In addition to the standard title check, you must now investigate the insolvency status of the borrower/guarantor:

Search NCLT Filings: Before placing a bid, check the National Company Law Tribunal (NCLT) cause lists and e-filing portals for the specific city. Look for applications filed under Section 94 (by the debtor) or Section 95 (by a creditor) against the owners.

Check IBBI Records: The Insolvency and Bankruptcy Board of India (IBBI) maintains records of ongoing insolvency processes. Verify if the borrower's name appears in any public notices.

Ask for a "No-Insolvency" Declaration: Demand that the Bank’s Authorized Officer provide a written statement confirming that, to the best of their knowledge, no insolvency proceedings have been initiated as of the auction date.- Strategic Payment Timing

The court ruled that ownership only transfers at the moment the Sale Certificate is issued.

Push for Immediate Issuance: Under SARFAESI Rule 9, the balance 75% is usually paid within 15 days. Aim to pay this as quickly as possible and insist that the Bank issue the Sale Certificate the same day you complete payment.

Avoid Extensions: Do not ask for the 90-day payment extension unless absolutely necessary. Every day you wait is a day the borrower has to file for insolvency and trigger an automatic stay.- “Double-Check” on the Final Payment Date

On the day you are about to pay the final 75% of the bid amount:

Perform one last search of the NCLT filing system.

If a moratorium has been triggered that morning, the Bank is legally barred from accepting your money. If they accept it anyway, your funds could be tied up in litigation for months or years.- Inclusion of “Refund Clauses” in the Sale Terms

While most bank auctions use standard “As-is-where-is” documents, you can try to submit a letter along with your EMD (Earnest Money Deposit) stating that:

The bid is subject to the property being free from IBC Moratoriums.

In the event of a legal stay under Section 96 of the IBC, the Bank must refund the entire deposit with interest within a specified timeframe (e.g., 15 days).- Immediate Possession Strategy

The Arrow Business case showed that the purchaser lost because they had the certificate but not the possession when the stay was analyzed.

If you successfully get the Sale Certificate, move for physical possession immediately.

If the property is vacant, ensure the bank hands over the keys at the same time the certificate is signed.

Summary Checklist for Purchasers

| Stage | Action |

| Pre-Bid | Check NCLT/IBBI for any Section 94/95 filings against the borrower. |

| Auction Day | Verify if any stay was granted by the DRT or NCLT that morning. |

| Post-Auction | Pay the 25% and immediately verify the timeline for the final 75%. |

| Final Payment | Check NCLT again -> Pay 75% -> Get Sale Certificate instantly. |

Join our Whats app Channel Whats App Channel :

https://whatsapp.com/channel/0029Va4QnQXKQuJDKzWgtp1F

Like our Facebook page https://www.facebook.com/propheadlines/

For Latest Real Estate Investment News Log on to https://propheadlines.com/

Our Project Posting page https://propheadlines.net/

{kind=link}